In the year of 2022, the S&P BSE Sensex touched a low of 51,360 and a high of 63,284, and delivered just 4 percent returns in the calendar year. How do you make money amid such volatility? Balanced advantage funds were touted as one of the solutions.

These funds invest across equity and debt markets, but toggle between the two depending on the valuations. The beauty of Balanced Advantage funds (BAF) or dynamic asset allocation funds as they also called, is that they give you a tax advantage as the net exposure in equities is at least 65 percent. The raw equity exposure could go down to as low as 30 percent (if fund managers believe that equity markets are over-valued), but they use derivatives to bring up the equity exposure to qualify as an equity fund, from a tax point of view.

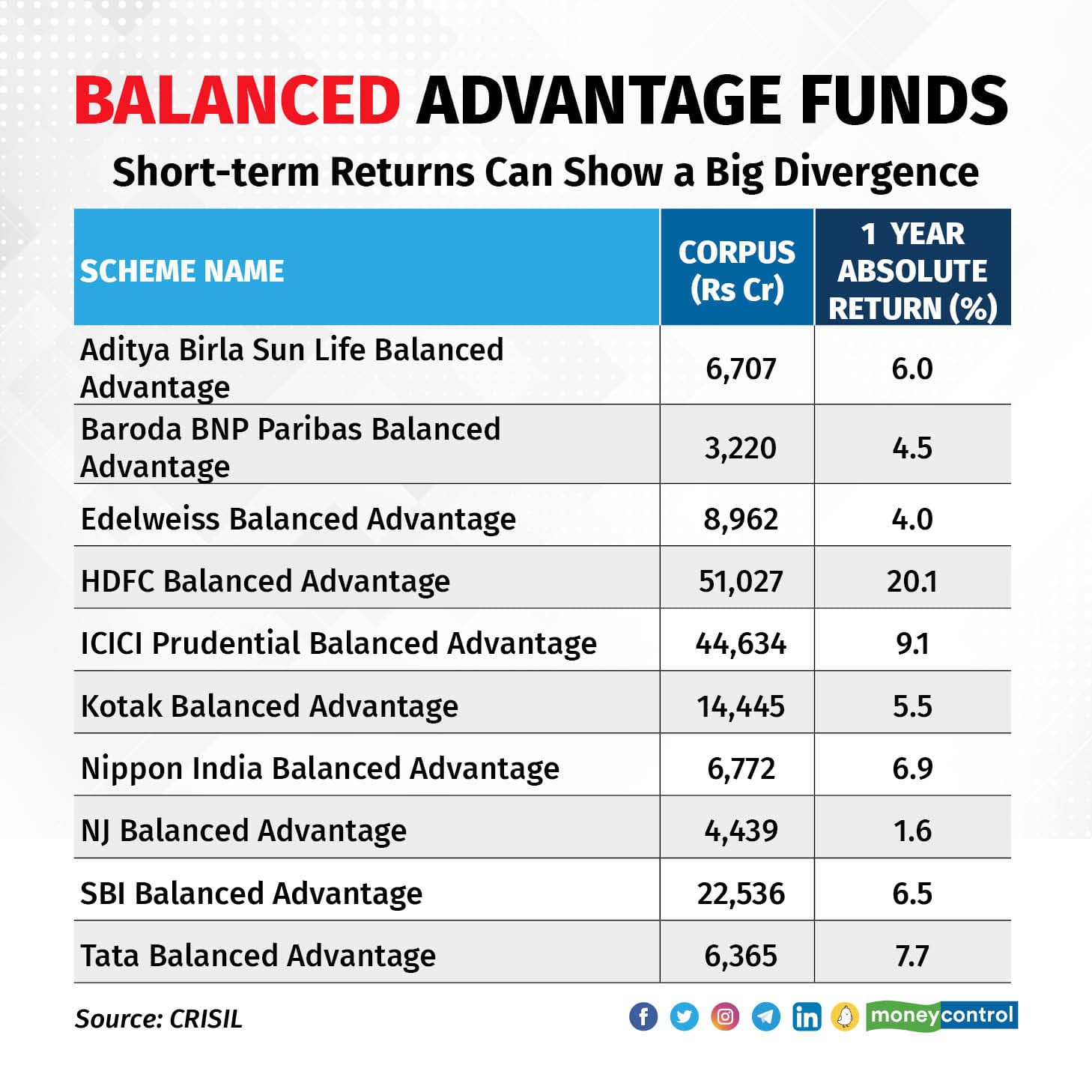

Did BAFs deliver?

Short-term returns can show a big divergence like they did in 2022.

Short-term returns can show a big divergence like they did in 2022.

In 2022, 10 of the largest schemes in the category returned between 2-20 percent. Such a variance can make it challenging when deciding which BAF to pick for your long-term portfolio.

What caused this sharp variance in returns?

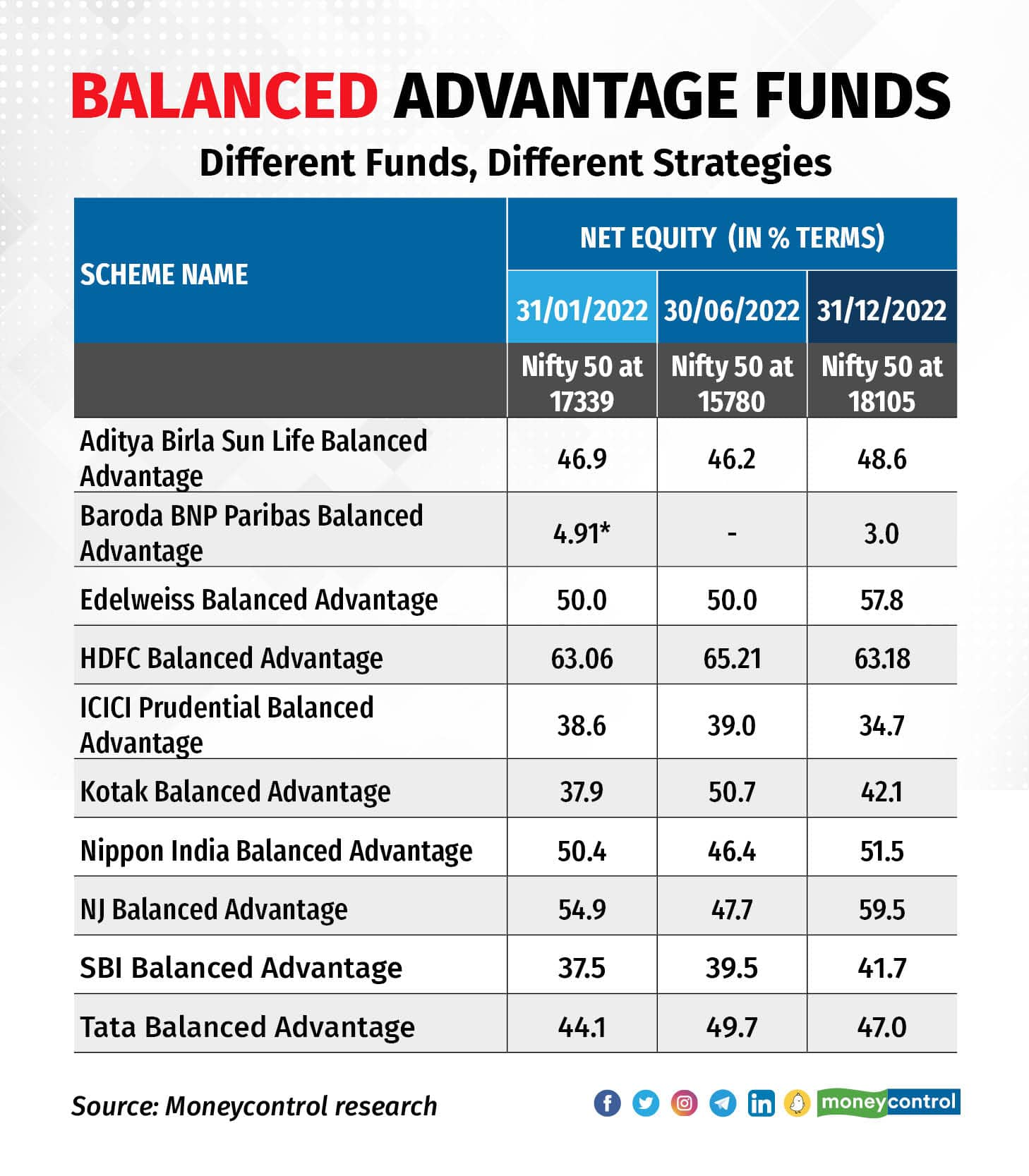

No two BAFs are the same

If you look at the net equity exposure across three of the largest schemes, the variance is significant and shows a difference in approach in the asset allocation strategy. This could well be a contributor for the divergence in returns.

Balanced Advantage Funds come in different hues; in terms of equity exposure and also how much equities they hold; both at the lower and higher side

Balanced Advantage Funds come in different hues; in terms of equity exposure and also how much equities they hold; both at the lower and higher side

According to Piyush Gupta, Director, Funds Research, CRISIL Market Intelligence and Analytics, “Within equity, the framework of these funds is such that when markets are overvalued, the hedged portion of the equity portfolio goes up, and vice-versa. It’s the net equity exposure, or the unhedged portfolio, that determines the performance. If the framework underlying the portfolio construction of a fund is able to accurately capture the valuation shifts in the equity market, performance over time will look favourable.”

It doesn’t make decoding a BAF any easier when each fund has a different framework and, in some cases, the net equity position remains in a tight range despite changes in market valuation. For example, the Edelweiss Balanced Advantage Fund applies a pro-cyclical approach, which means that it keeps the asset allocation in line with the market cycle: increasing exposure in a rising market and reducing in a falling market. Along with this, market health and overriding factors are analysed to decide how much needs to be allocated to equity. Counter-cyclical strategies like the ones used by ICICI Balanced Advantage Fund or SBI Balanced Advantage Fund do the opposite.

According to Niranjan Avasthi, Senior Vice-President and Head, Product, Marketing and Digital, Edelweiss Asset Management, “Back-tested data of the last two decades shows that aligning asset allocation with the market trend helps the portfolio outperform the broader markets for a larger portion of time. In a growth market like India, this strategy helps capture the upside better. However, during periods where the trend is volatile or flat, the strategy may temporarily remain an average performer rather than an outperformer.”

The opposite of this is a counter cyclical strategy, where exposure to equity assets is reduced when the market keeps rising relentlessly in a short span, making valuations expensive, and increased when the market corrects.

Some funds rely more on the fund manager’s discretion.

“The framework we use for our fund reduces allocation to equity when valuations are expensive relative to fixed income or when sentiment is unusually euphoric, and vice versa. From the time we have launched the fund, the framework has not supported higher equity allocation either on account of relative valuations or sentiment. Asset allocation can be modelled around various strategies, this is the one that we chose with the objective of delivering stable risk-adjusted returns and downside protection over long periods,” says Dinesh Balachandran, Fund Manager, SBI Mutual Fund.

These different approaches to deciding asset allocation in a dynamic fund like BAF is one of the primary reasons for the variance in returns which we saw in 2022. While the asset allocation strategy is important, portfolio composition matters too.

Take the HDFC Balanced Advantage Fund, which has the highest allocation to long equity. Banks are among its top holdings, with 15-20 percent exposure through the year across 2-5 stocks. Banking was one of the best performing sectors in 2022. The Bank Nifty index delivered around 18 percent for the year compared to the Nifty50’s 2.7 percent.

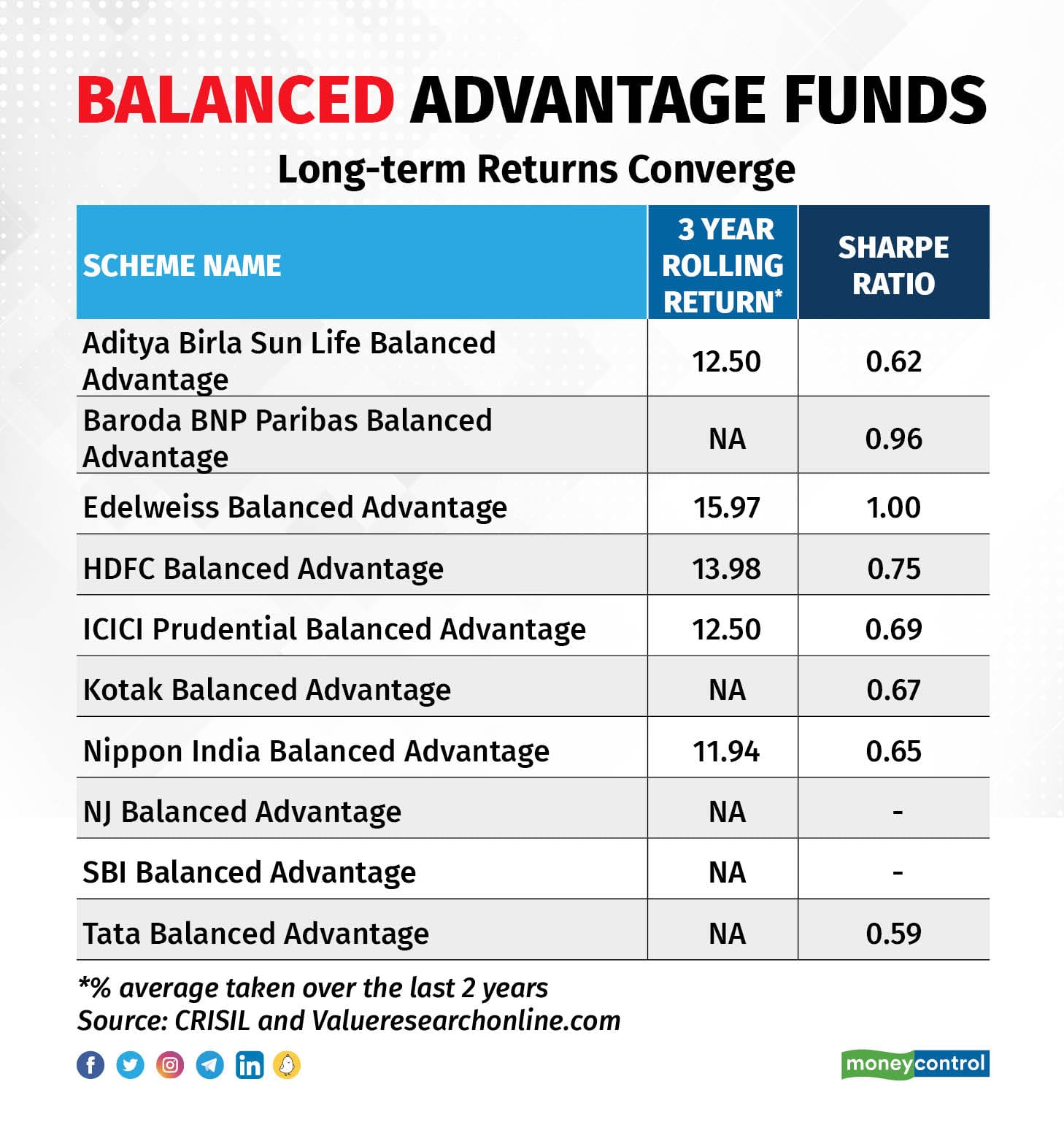

Zoom out

Zoom out slightly and look beyond the calendar year, see the three-year rolling returns over the last two years. Basically, returns for a period of three years seen every day over the last two years. The average of such returns for the top 10 schemes (by assets under management) in the category shows a lot more convergence. The average three-year rolling returns fall squarely in the 12-16 percent range, annualised.

Although Balanced Advantage Funds follow different strategies to make the most of equity markets, their long-term returns usually converge

Although Balanced Advantage Funds follow different strategies to make the most of equity markets, their long-term returns usually converge

Avasthi says, “Our framework for the fund works to limit the downside while capturing a higher degree of the upside. On a three-year rolling return basis, there has been no negative returns.”

It is not easy for individual investors to judge the ability of a fund to do this just by reading the investment strategy or even by knowing the framework for dynamic asset allocation.

Matching fund returns and asset allocation with the market movement over 3-5 years can show which funds are delivering stability along with favourable participation in the upside.

Gupta says, “The consistency with which the model or framework underlying the scheme is able to match the movement in market prices is going to determine how well these schemes perform across longer periods of time. Ideally, the objective should be to have stable long-term returns, or in other words, lower volatility than pure equity exposure, and appropriate capture of upside returns.”

Figuring this out is not an easy task. Between January 15 and March 23, 2020, when the market corrected sharply and fell roughly 40 percent, BAFs fell by 12-33 percent. One BAF that followed a pro-cyclical strategy fell by around 14 percent, while another that followed a counter-cyclical strategy fell by around 26 percent. The worst-performing fund in this period was one where the fund manager’s discretion reigned supreme.

Over the next one year, the Nifty 50 gained roughly 65 percent and funds in this category delivered returns in the range of 25-75 percent. The one which lagged the others earlier turned around and topped the charts.

All this might be a bit baffling when it comes to picking the so-called best BAF. The schemes with the highest returns may not be your first choice, if returns are volatile. Thus, schemes with relatively lower returns may offer the stability you seek across different periods of time.

BAF or no BAF? What should investors do?

The premise of a BAF is to participate in equities while protecting the downside in volatile times. This means your BAF must give returns in excess to that of debt funds and fixed deposits.

Given that BAFs follow a variety of strategies, you might not get your desired results in a shorter time frame, say 6-12 months. Hence, it’s best not to come to a conclusion about your BAF by looking at short-term returns. Remember, at heart, these are equity-oriented funds, but with a bit of flexibility to help maximise returns.

Just ensure that the BAF you choose has a stable return over a 3–5-year period, preferably, with lesser volatility than an equity fund.

Do your homework. Not all BAFs are the same. Even BAFs can be volatile, but how much of that you’re comfortable with will depend on your investment style.

Just because a BAF toggles between equity and debt to protect the downside and benefit from the upside doesn’t mean that you should put all your money in one such scheme and expect your portfolio to be taken care of. Most financial experts say one fund that follows an automatic asset allocation strategy is good enough. For the rest of your portfolio, your planner or you could take care of the asset allocation.