The survey, carried out in partnership with data analytics firm Kantar, shows that urban India is more aware about life insurance products in the market and a larger chunk of this population owns life insurance policies, compared to IPQ 1.0, carried out in 2019.

Indians are more aware about their financial security and preparedness since the COVID-19 outbreak in 2020, as there is a significant shift towards increasing savings and investments.

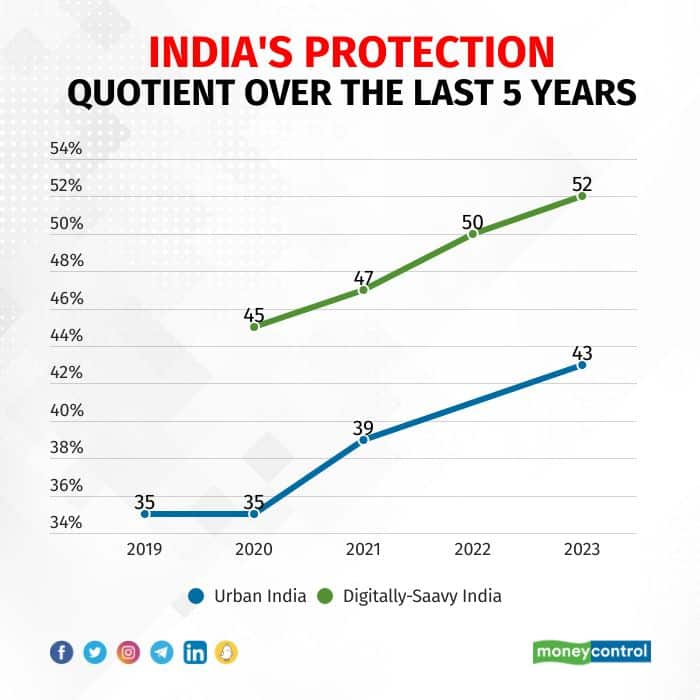

According to the fifth edition of the India Protection Quotient (IPQ) Survey by Max Life Insurance, which covered 4,610 respondents across the offline and digital categories, on a scale of 0 to 100, the degree to which Indians feel protected from future uncertainties has increased four points from 2020 to 43 now.

The survey, carried out in partnership with data analytics firm Kantar, shows that urban India is more aware about life insurance products in the market and a larger chunk of this population owns life insurance policies, compared to IPQ 1.0, carried out in 2019.

The urban India has achieved pre-covid levels of financial protection.

The urban India has achieved pre-covid levels of financial protection.

The security levels in the country, a degree to which Indians feel financially secure and prepared, has risen six points since the last survey. The COVID-induced fears still keep it below the levels reported in IPQ 1.0.

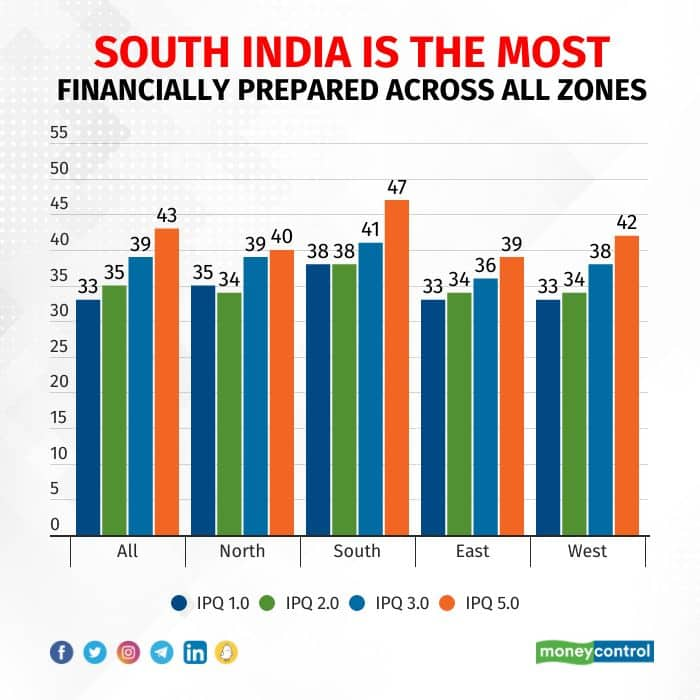

While the whole of India has performed well on its protection quotient survey, south India celebrates an undisputed first across all zones for the fifth consecutive year, with eight out of 10 individuals owning a life insurance policy.

It has seen more than a 23 percent rise in its protection quotient since 2019. While the awareness levels have increased the most in the northern and western parts of India, security levels have struggled to catch up to pre-pandemic times.

South India, which has seen around a 7 percent rise in people feeling financially secure and prepared, stands as an exception in this category.

South India remains at the top in terms of financial protection for the 5th consecutive year.

South India remains at the top in terms of financial protection for the 5th consecutive year.

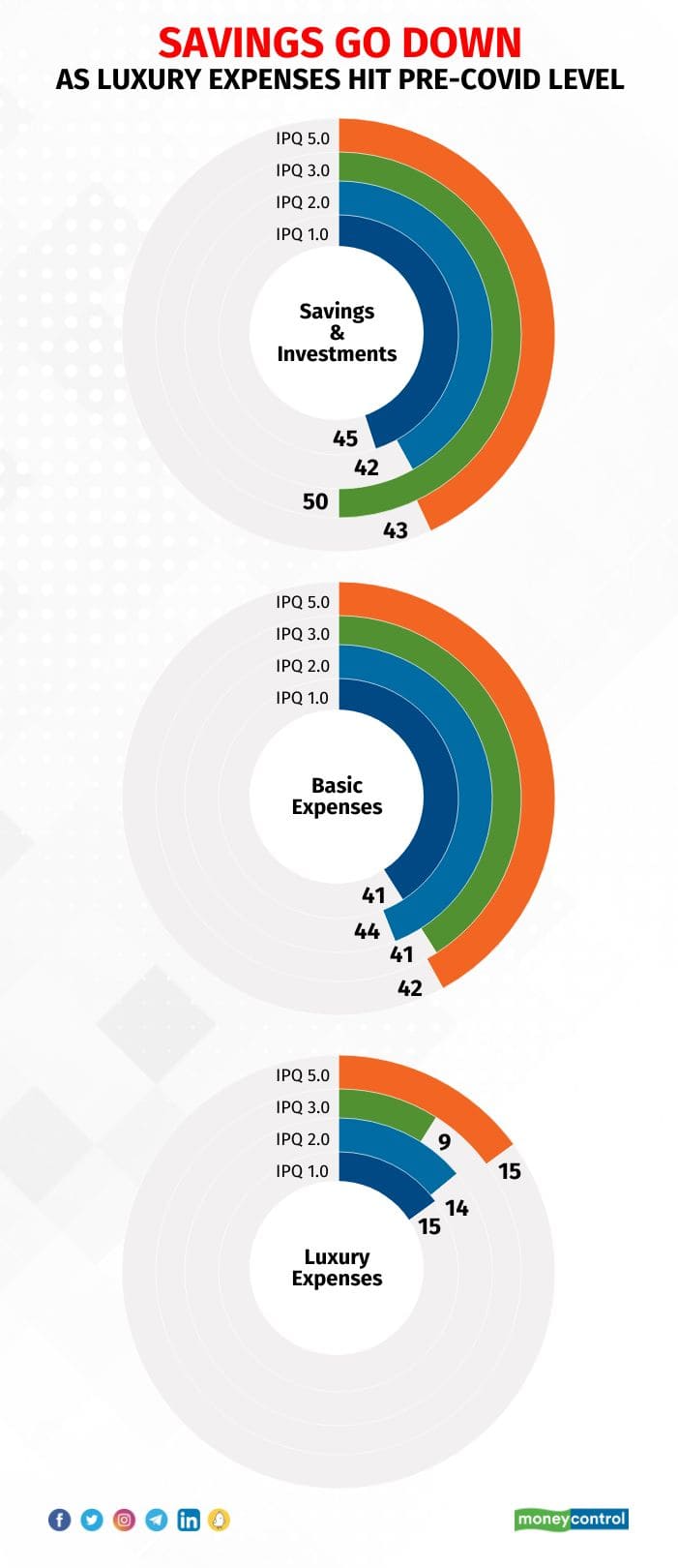

Luxury spending rises, savings fall

Luxury spends have gone back to the pre-COVID levels while savings and investments have taken a hit and stand at 43 percent. Savings for milestones, such as kids’ education and marriages, have gained the most traction as the savings objective.

But most people have reported ‘planning for uncertainties’ as the least preferred saving goal, in a scenario where 64 percent of urban Indians feel that inflation has emerged as the predominant concern.

The savings and investment sentiment amongst the households fall as the luxury spends resest to pre-pandemic levels.

The savings and investment sentiment amongst the households fall as the luxury spends resest to pre-pandemic levels.

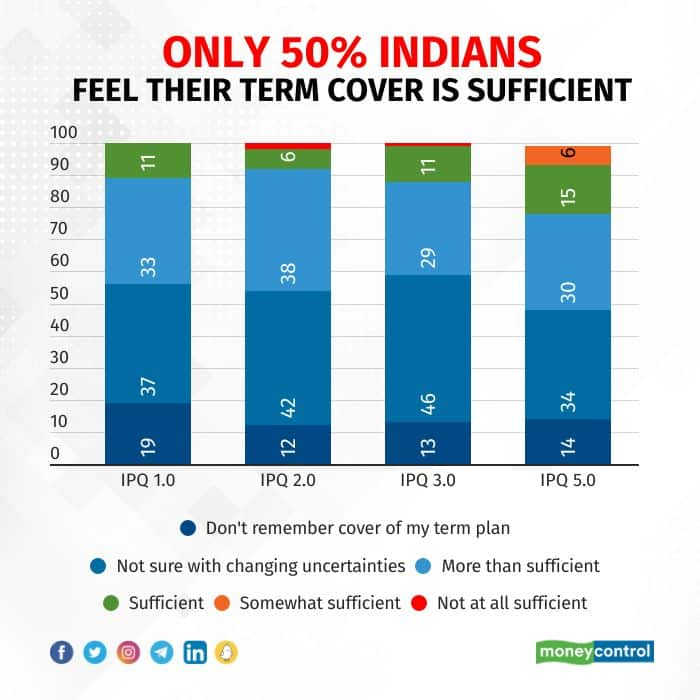

With awareness around term insurance at an all-time high of 64 percent, more consumers prioritise sum assured and rider benefits while purchasing a term product. But only one in two Indians feel their term insurance cover is sufficient for them.

While people in Tier 1 cities have outpaced their peers in metros, in terms of owning a term insurance policy, increased inflationary pressures make it harder for them to predict the quantum of corpus needed.

half of the Indians feel that their term cover is insufficient amidst the increasing healthcare rates and risks.

half of the Indians feel that their term cover is insufficient amidst the increasing healthcare rates and risks.

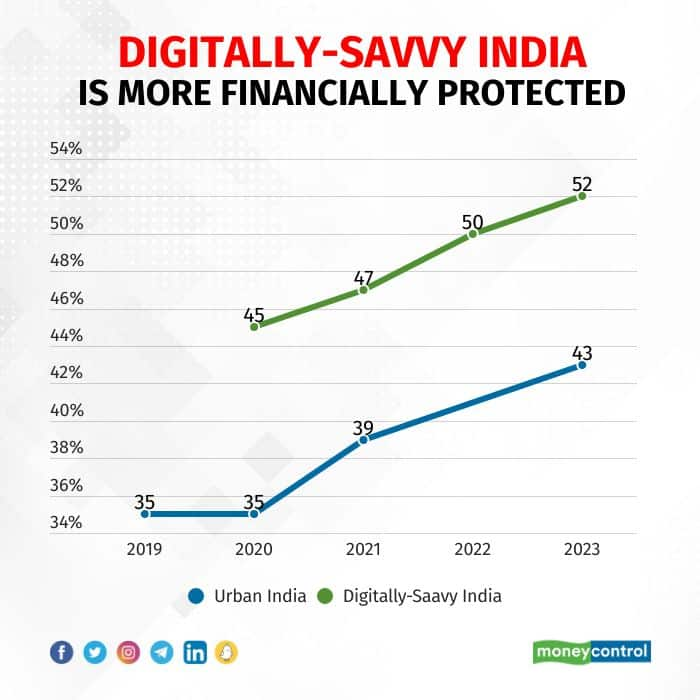

Digitally-savvy population feel more secure

More than half of the digitally-savvy population feels more secure and aware about their financial protection. Though the Tier 1 population saw the highest spike in owning a term insurance product in the offline insurance market, Tier 2 cities have topped ownership and security levels in the digitally savvy consumer base of the insurance industry. This signifies that a better infrastructure can help penetrate the financial protection to a wider population of India.

Digitally-savvy Indians feel more financially protected as compared to the offline consumers of the insurance industry.

Digitally-savvy Indians feel more financially protected as compared to the offline consumers of the insurance industry.

While urban India has come a long way with regards to being more financially aware and taking steps to feel more secure about their future, the gap of awareness between the salaried and self-employed class, and men and women still needs to be bridged.