SEBI is contemplating reducing a mutual fund's Total Expense ratio, for larger fund houses

Capital market regulator Securities and Exchange Board of India (Sebi) is planning to prevent large mutual fund (MF) houses from charging high expense ratios.

In December 2022, the market regulator announced that it has initiated an internal study to re-look at the expenses that fund houses charge unitholders.

Moneycontrol has now learnt that Sebi may put a threshold on the overall equity assets under management (AUM) of fund houses to determine the expense ratio it can charge its investors.

For instance, if a fund house’s equity AUM is Rs 50,000 crore (a figure that Sebi appears to be ideating around), then the fund house’s existing schemes as well as new schemes would be made to charge a lower expense ratio, compared to what they are qualified for under the present norms.

Moneycontrol has learnt that the new expense ratio for such fund houses may likely be either 1.25 percent or 1.50 percent.

Sebi appears to have analysed MF inflow data and observed that when fund houses, especially large and mid-sized ones, launch new schemes, some distributors take their investors’ money out from existing schemes and put it in new schemes. This enables the distributors to earn a higher commission as newly-launched schemes can pay higher distribution fees.

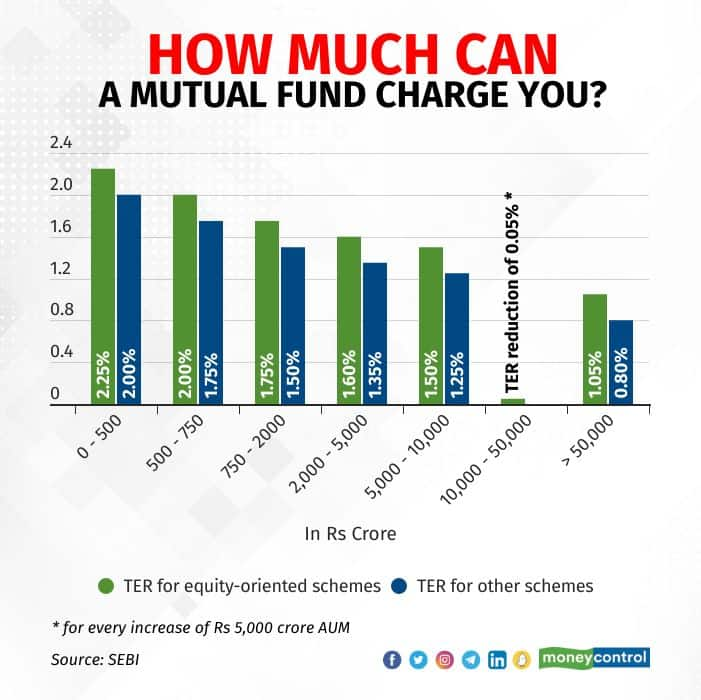

As per Sebi's present formula, schemes with an AUM of up to Rs 500 crore can charge total expense ratio (TER) of up to 2.25 percent. As the scheme grows in size, its TER comes down <see table>. SEBI’s 2018-updated TER formula accounts for a scheme’s burgeoning size; a major upgrade to its age-old formula.

SEBI's present-day formula for mutual funds to charge fees to unit holders.

SEBI's present-day formula for mutual funds to charge fees to unit holders.

But some things didn’t change.

Sebi has observed that new schemes still get to charge higher TERs. This is the case with large fund houses as well. While large fund houses may have schemes in excess of Rs 20,000 crore, their newly-launched schemes charge TER of up to 2.25 percent. On the face it, nothing appears to be wrong here.

But some distributors are incentivised to shift investors from a larger scheme of the same fund house to its newly-launched scheme. Money remains within the fund house, but the investor pays more for the shift. Distributors who indulge in such practices make a fast buck at the expense of the investor.

Sebi has observed such churn in regular (distributor) plans, and not in direct plans. This further points to the mischief, believes SEBI.

Besides lowering the TER, Sebi is also contemplating removing exemptions. In simple words, either the small-town penetration incentive of 30 basis points (bps) might be abolished, or it could be brought within the TER that the scheme charges. One basis point is 1/100th of a percentage point. At present, schemes can charge an additional 30 bps over and above the TER, if it gets a certain percentage of its corpus from beyond the largest 30 towns. In MF parlance, this is known as the B30 incentive.

Fund houses also pay Goods and Services Tax (GST) to the government on the Investment Management fee that it collects. This falls within a scheme's TER that it collects, and is usually up to 60-70 bps. As per present norms, GST is over and above the TER it charges. Now, SEBI plans to bring GST within the TER.

But the most drastic change that it is contemplating it that to bring the transaction costs within the TER. Fund houses pay brokerage costs to stock brokers every time they buy and sell securities. This cost (0.12 percent) is per trade and presently sits outside a fund's TER. Sebi might bring this inside a scheme's TER. This, say industry officials, will hit an asset management company's profitability hard as it would then be linked to a fund's corpus.

All of the above moves will reduce a fund house’s ability to pay to distributors.

It is unclear if Sebi will restrict the expenses to new as well as existing schemes, or just the new schemes that the large fund houses launch. It is also not clear if SEBI’s new strictures on expense ratios would apply to only equity schemes or all schemes. SEBI is still at the consultation stage. Later, it is expected to bring out a consultation paper and seek public opinion. Post that, SEBI might issue detailed guidelines. We’re still a few months away from that.